Australian Climate-Related Financial Disclosures Under AASB S2 — Done For You, Audit-Ready

From 1 January 2025, large Australian businesses are legally required to prepare and lodge climate-related financial disclosures under AASB S2 and IFRS S2 — the Australian Sustainability Reporting Standards (ASRS).

The obligation applies in phases across three groups, with penalties for non-compliance enforced by ASIC. Carbonhalo delivers complete, audit-ready climate disclosures — built for businesses reporting for the first time. No in-house sustainability team required. No jargon. Fixed-price, expert-led, and compliant.

What Is AASB S2?

AASB S2 is the Australian Accounting Standards Board’s climate-related disclosures standard. It forms part of the Australian Sustainability Reporting Standards (ASRS) and requires large Australian entities to disclose information about their exposure to climate-related risks and opportunities.

AASB S2 was introduced by the Treasury Laws Amendment (Financial Market Infrastructure and Other Measures) Act 2024 and is substantively aligned with IFRS S2 — the global climate disclosure standard issued by the International Sustainability Standards Board (ISSB).

What must be disclosed under AASB S2?

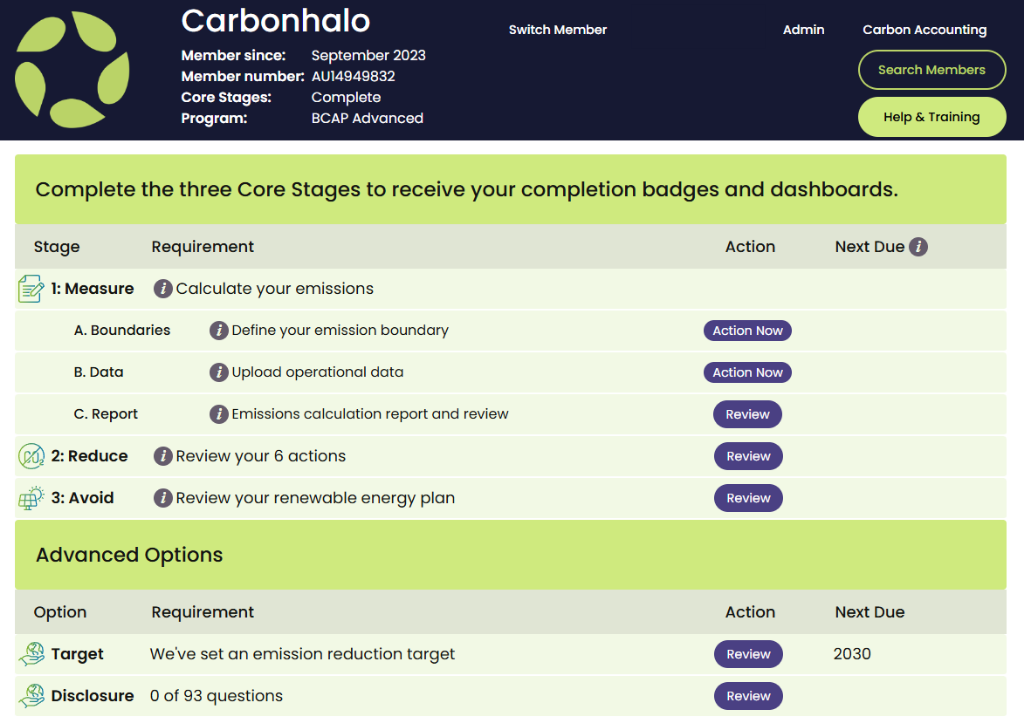

AASB S2 requires disclosures across four interconnected areas:

Pillar | What it Requires | Example Disclosures |

|---|---|---|

1. Governance |

How the board and management oversee climate-related risks and opportunities |

Board committee responsible for climate; frequency of climate reporting to board |

2. Strategy |

How climate risks and opportunities affect your business model, strategy and financial planning |

Physical risks to key assets; transition risks from policy change; climate scenario analysis |

3. Risk Management |

How you identify, assess and manage climate-related risks |

Integration of climate risk into your enterprise risk management framework |

4. Metrics & Targets |

Scope 1, 2 and 3 emissions data and your emissions reduction targets |

Total tCO₂e per Scope; net zero target; emissions intensity ratios |

Scrolls right for more data ->

What is the difference between AASB S2 and IFRS S2?

IFRS S2 is the global climate disclosure standard issued by the ISSB. AASB S2 is Australia’s adoption of that standard — it is substantively identical in disclosure requirements but is the legally binding version for Australian reporting entities. AASB S2 includes Australian-specific transitional provisions, modified safe harbour liability protections, and is enforced by ASIC and the AUASB.

If you are an Australian entity, you comply with AASB S2. If you are reporting to international investors or a global parent, you may also need to reference IFRS S2.

Which Climate Reporting Group Are You In?

Understanding your business classification within the Mandatory Climate Related Financial Disclosures is the first step. Programs are designed for Australian businesses based on your compliance timeline and reporting complexity.

Group 3

- Revenue > $50M

- Assets > $25M

- Employees > 100

Guided preparation

and roadmap delivery

No Experience Required

We understand that many businesses are new to mandatory climate-related financial disclosures. That’s why Carbonhalo is built specifically for companies that don’t have in-house sustainability teams, are unsure where to start, and want compliance without complexity.

No In-House Teams

Don’t have sustainability experts? No problem. We become your outsourced compliance and climate reporting team.

Unsure Where to Start

We guide you through every step, from baseline carbon disclosure report, gap assessment to final disclosure.

Compliance Without Complexity

We become your ASRS Climate reporting partner that speaks your language.

Baseline Emissions Assessment

Complete Scope 1, 2, and 3 emissions measurement using ISSB-aligned methods

Gap Analysis and Disclosures

Comprehensive review against IFRS S2 and AASB S2 requirements

ISSB-Aligned report Pack

Complete sustainability report ready for board and regulator submission

Australian Built. Trusted Experts. Real Results

Unlike overseas software or generic consultants, Carbonhalo is proudly Australian. Our experts come from and know the Australian business landscape, producing Australian Climate Disclosure reports across multiple industries.

Human

On-ground support across Australia. Face-to-face with real people.

Trusted by

Australian Businesses

Built For Australian Businesses

Built for First-Time Reporters

Designed specifically for

companies new to

climate compliance

Done-for-You

Model

You focus on your business.

Mandatory climate-related financial disclosures sorted by us.

Affordable &

Flexible

Monthly pricing with

no lock in contracts or

annual price shock.

Project Managed

We set a schedule and keep stakeholders on track

Trusted by Corporates

Used by businesses meeting

legislative thresholds across

Groups 1, 2 and 3

Australian Expertise

Access to industry experts

is all-inclusive with

no consulting fees

Frequently Asked Questions: Financial Disclosures Under AASB S2

Regulatory & Compliance Questions

AASB S2 is the Australian Accounting Standards Board’s Climate-related Disclosures standard, part of the Australian Sustainability Reporting Standards (ASRS). It requires large Australian entities to disclose climate-related risks and opportunities across four areas: Governance, Strategy, Risk Management, and Metrics & Targets. It is substantively aligned with the global IFRS S2 standard issued by the ISSB.

Australian entities required to prepare financial reports under the Corporations Act 2001 that meet two of three size thresholds. Group 1 (revenue >$500M, assets >$1B, or employees >500) must comply from FY2025. Group 2 (revenue >$200M, assets >$500M, or employees >250) from FY2026. Group 3 (revenue >$50M, assets >$25M, or employees >100) from FY2027.

IFRS S2 is the global climate disclosure standard issued by the International Sustainability Standards Board (ISSB). AASB S2 is Australia’s legally binding adoption of that standard. They are substantively identical in disclosure requirements. The key differences are that AASB S2 includes Australian-specific transitional provisions, modified safe harbour protections, and is enforced by ASIC.

For Group 1 entities with a 31 December 2025 financial year-end, the first climate disclosure must be included in their annual report lodged in early 2026. Group 2 entities first report for financial years beginning on or after 1 January 2026. Group 3 entities first report for financial years beginning on or after 1 January 2027.

Yes, if they are required to prepare financial reports under the Corporations Act 2001 and meet two of the three size thresholds. The obligation applies to large proprietary companies, public companies, and registered managed investment schemes — not just ASX-listed entities.

Non-compliance is enforced by ASIC under the Corporations Act. Penalties can include civil penalties for directors, infringement notices, and reputational consequences. ASIC has signalled active enforcement of climate disclosure obligations. First-year reporters who make good-faith attempts at compliance and disclose limitations transparently are generally treated more favourably.

The safe harbour provision protects entities from civil liability for forward-looking climate-related statements made in good faith in their first three years of reporting (Group 1 and 2) or first year (Group 3). It applies to statements about future strategy, scenario analysis and transition plans — not to historical emissions data or factual matters, which must be accurate.

AASB S2 builds on and supersedes the TCFD (Task Force on Climate-related Financial Disclosures) framework. If your business has previously reported under TCFD, you will find the four disclosure pillars familiar — but AASB S2 is more prescriptive, includes mandatory Scope 3 consideration, requires scenario analysis, and has legally binding force.

Process & Technical Questions

The core data requirements are: 12 months of energy consumption data (electricity bills, gas invoices, fuel records); fleet vehicle distances and fuel types; refrigerant purchase and top-up records; business travel records (flights, accommodation); waste disposal records; and details of major suppliers and purchased goods. Carbonhalo provides a structured data collection template to guide this process.

A baseline emissions assessment is a comprehensive measurement of your organisation’s greenhouse gas emissions across Scope 1 (direct emissions), Scope 2 (purchased electricity) and Scope 3 (value chain emissions). It establishes a reference year against which future emissions reductions are measured. Under AASB S2, your baseline assessment must use GHG Protocol or ISO 14064 methodology with ISSB-aligned emission factors.

Yes — AASB S2 requires all groups to assess the resilience of their strategy under climate scenarios. The standard requires at least two scenarios: typically a 1.5°C or well-below 2°C transition scenario and a physical risk scenario. However, first-year reporters can use qualitative scenario analysis, and Group 3 entities have a simplified pathway. Carbonhalo guides you through scenario analysis appropriate to your entity size and industry.

For a first-time reporter using Carbonhalo’s done-for-you service, the typical timeframe is 3–5 months from engagement to a lodgement-ready report. This includes data collection (4–6 weeks), baseline assessment and gap analysis (3–4 weeks), governance and strategy drafting (4–6 weeks), and report preparation and review (3–4 weeks). Group 1 entities with urgent deadlines can access an accelerated pathway.

Carbonhalo's Committment

Carbonhalo’s compliance service includes: Group classification and compliance brief; data collection template and guided collection process; baseline Scope 1, 2 and 3 emissions assessment; climate risk and materiality assessment; governance and strategy disclosure drafting; gap analysis against AASB S2 requirements; complete audit-ready AASB S2 report; limited assurance documentation pack (Groups 1 and 2); and lodgement support. All work is performed by our Australian team of carbon accountants and regulatory specialists.

Yes. All emissions calculations include full working papers, source data references, calculation methodology notes and emission factor citations — formatted for review by your external assurance provider. For Group 1 and 2 entities requiring limited assurance, we prepare the documentation structure required by AUASB standards.

Yes — this is specifically what we are built for. Over 700 Australian businesses have used Carbonhalo without any prior sustainability expertise or in-house resources. We act as your outsourced climate compliance team: collecting data, performing all analysis, drafting all disclosures, and managing the process from start to lodgement.

Carbonhalo offers monthly pricing with no lock-in contracts. Pricing is based on your Group classification, entity complexity and scope of service. We provide a fixed-price quote during your free Compliance Plan session — before any commitment. There are no hidden fees, no time-and-materials billing, and no annual price shock.

Real Results From Businessess Like Yours

Let’s Make Climate Compliance One Less Thing to Worry About

- Confirm your Group classification

- Understand your requirements in plain language

- Get a clear, fixed-price quote

- See how we make the process simple

Book Your FREE Personalised Compliance Plan

Real one-to-one expert session

Your information is secure and will never be shared.